- Charts of the Day

- Posts

- Higher oil prices could reignite inflation.

Higher oil prices could reignite inflation.

But “Iran” unlikely to dent bullish view.

1. High crude prices could hit global growth and would push inflation expectations higher.

This will reduce any expectations of more Fed rate cuts in 2026.

2. “Iran” unlikely to dent bullish view.

JPMorgan said the weekend’s events will naturally lead to risk-off in the short term, but investors with a 3/6/12-month time frame should use weakness to increase exposure. Morgan Stanley agrees that the bullish view is intact for now, with a lasting spike in oil above $100 needed to impact the US equity outlook.

The impact on the stock market will be determined by its duration, Citigroup strategists said, as they presume a shorter-term impact.

Both earnings and profit margins hit new highs last week. Hard to get overly bearish when this is happening.

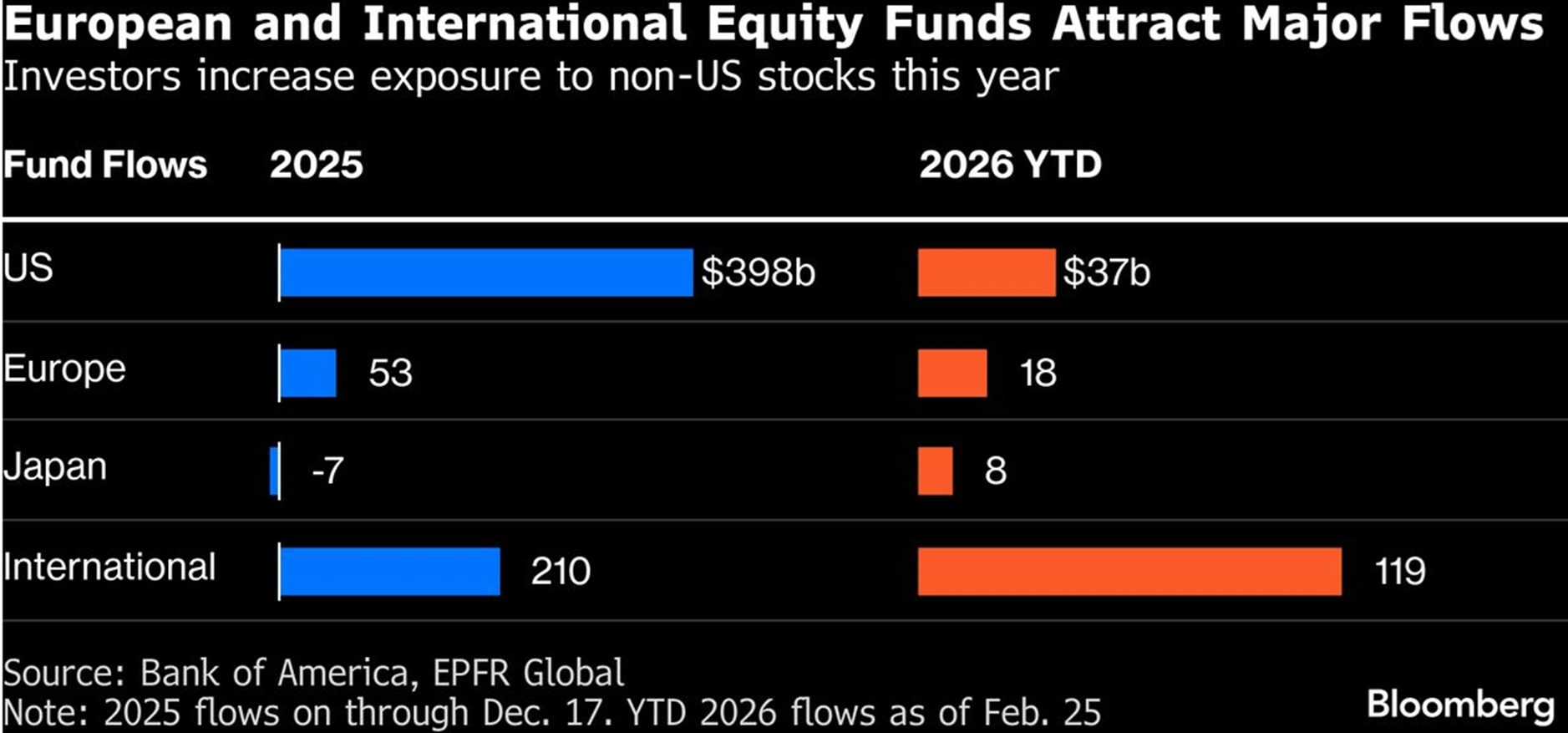

3. However, geopolitical events underscore the need to diversify away from the US.

It’s not just geopolitics that’s prompting diversification. Worries over AI spending are encouraging rotation from the US to other regions. So far this year, old-economy sectors like basic resources, energy, telecommunications and utilities have outperformed, posting double-digit returns of as much as 22% while the Stoxx 600 gained 7%.

Funds focused on international and European equities continue to attract inflows faster than the US. New money is being allocated in a completely different way to last year, backing a trend of outperformance in benchmarks from outside the US.

4. A record run of buyback announcements is another reason for investors to buy European stocks and diversify their exposure outside the US.

Members of the Stoxx Europe 600 index have announced €85.7 billion of share repurchases, the highest ever for the January-February period, according to a Barclays tracker.

On top of that, around 76% of buyback plans authorized by shareholders have yet to be carried out, leaving plenty of dry powder to support flows into the second quarter.

5. Quo vadis Nvidia?

For the last two quarters NVIDIA has not moved while business has continued to strengthen - a function of concerns about the durability of current growth.

The bear case argues that specialized custom chips would steal the inference market. Nvidia’s response is a shift from selling individual chips to delivering entire AI Factories. By controlling the networking fabric and the software stack, Nvidia is ensuring that the cost-per-token remains lower on its platform.

Also, margins are the ultimate lie detector: Despite the complexity of ramping liquid-cooled Blackwell racks and the surging cost of memory chips, gross margin improved to 75.2%. If demand were softening or competition were biting, this would be the first place we would see scuff marks.

Big picture: Nvidia’s engine is now powered by the Blackwell Ultra refresh, the explosive networking growth, and the agentic transition. With $95 billion in supply-related commitments on the books, Nvidia is already manufacturing the next two years of the AI cycle.

With the stock trading at 18x CY27 EPS, enthusiasm might come back sooner than later.

Not a subscriber yet?

How was today's Edition?What can we improve? We would love to have your feedback! |

Reply